Vincent Tan – The history and IPO of 7-Eleven Malaysia

By YEO Shan Rui

Tan Dato’ Seri Vincent Tan Chee Yioun (commonly known as Vincent Tan) is the owner of Cardiff City Football Club and the Berjaya Group in Malaysia. The success of his empire can be traced back to the untendered privatization of Sports Toto from the government of Malaysia in 1985 . Being one of three legalized lotteries operators, the cash flow has allowed him to diversify and build his conglomerate.

In the past 1 year, a number of his companies have attempted an IPO – Caring Pharmacy, Berjaya Auto, 7-Eleven Malaysia, MOL Global and Sports Toto Trust. While there have been speculation on the various reasons for the IPO spree, let’s focus our attention on 7-Eleven Malaysia.

Multiple rounds of listing and delisting

What’s make 7-Eleven Malaysia interesting was their history of numerous IPO and privatization attempts. Vincent Tan bought over the 7-Eleven franchise from Antah Holdings in 2001 through his Berjaya Group Berhad.

1st Round

In a restructuring exercise in 2004, 7-Eleven Malaysia was shifted to Intan Utilities which was also one of his public companies. In 2006, share price of Intan utilities spiked on announcement that they were buying 25.7% stake of Berjaya Sports. The deal was cancelled off and the share price languished. This led to the privatization of Intan Utilities at a PE ratio of 15.8x for RM 202 million. At that point in time, they had divested their utilities business and the core business was 7-Eleven convenience stores.

2nd Round

In August 2010, 7-Eleven was relisted together with Singer Group (deals with home appliances) under the company BRetail. The IPO price was RM 0.50 per share, representing a PE Ratio of 21.7 times for a market capitalization of RM 748 million. 9 months later, BRetail was delisted at a PE ratio of 18.6 times, representing a market capitalization of RM 973.3 million. Based on the offer document, the implied PE Ratio accorded to 7-Eleven Malaysia was 19.3x at an implied value of RM 547.2 million.

3rd Round

In November 2013, 7-Eleven Malaysia attempted an IPO again but was rejected by the Securities Commission of Malaysia. It was said that the rejection was due to the >30 x PE ratio valuation which was a huge jump as compared to the delisting in 2007 and 2011. The IPO was supposed to be US$700 million or RM 2.17 billion. In May 2014, 7-Eleven Malaysia was successfully listed at 33x 2013 earnings at the price of RM 1.38 per share and market capitalization of RM 1.7 billion. In the span of 3 years, valuation of 7-Eleven Malaysia has tripled. Of the RM 731 million raised in the IPO, the company received gross proceed of RM 250.3 million while the remaining RM 481.5 million was to the Selling Shareholder, BRetail. BRetail’s remaining 51% stake in 7-Eleven Malaysia is worth RM 850 million post-IPO.

Summary

In 2007, 7-Eleven was privatized at 15.8x PE for RM 202 million before relisted as BRetail at RM 748 million in 2010. 9 months later, BRetail was delisted at RM 973.3 million. In 2014, 7-Eleven was relisted at 33x PE for RM 1.7 billion. The cost for last round of delisting was close to the remaining stake in 7-Eleven Malaysia that BRetail owns. Therefore, BRetail nets a cash gain of RM 481.5 million and the Singer Group for free.

Related Parties Transaction

Source: 7-Eleven Malaysia’s IPO Prospectus

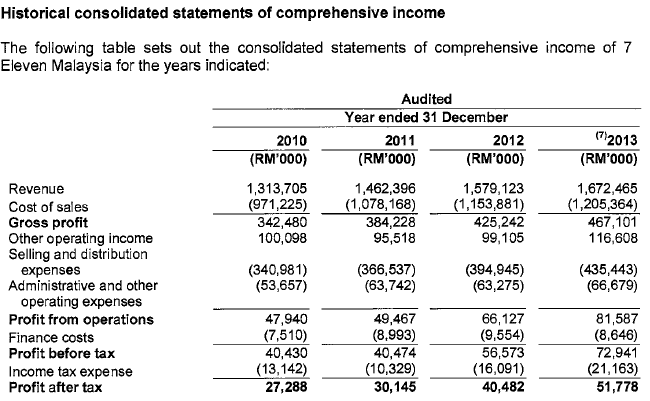

Notice that other operating income (RM 116 million) is actually larger than profit before interest and tax (RM 81.6 million). Some of these other operating income can include sub-rental, advertisement or even interest income.

Interest from advances to holding company

Source: 7-Eleven Malaysia’s IPO Prospectus

In 2013, interest income from “advances to intermediate and immediate holding companies” amounts to RM 14.5 million or 19.8% of Profit before Taxation. Where does this huge amount of interest income come from?

Source: 7-Eleven Malaysia’s IPO Prospectus

Apparently, 7-Eleven Malaysia has RM 177 million of loan provided to its holding company, BRetail, which then pays 7-Eleven Malaysia an interest rate of 5.8%. The loan will be paid off in the pre-ipo restructuring, so the RM 14.5 million of interest income will no longer exist post-IPO. Investors looking at the historical financial statement will have thought that the pro-forma net profit will be similar to RM 51.8 million, when in fact it should have been 20% lower.

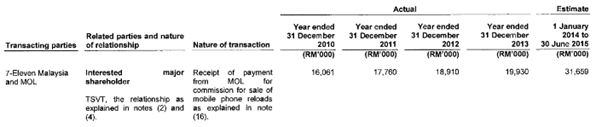

Commission Income from U Mobile and MOL Global

Source: 7-Eleven Malaysia’s IPO Prospectus

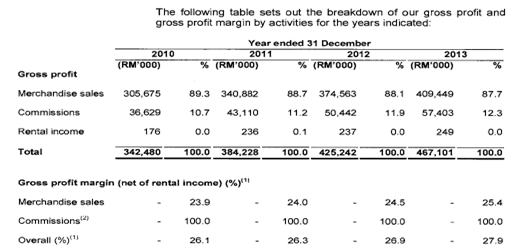

7-Eleven Malaysia is able to boast its increasing gross margin, which was due to commission income. Commission income, with gross margin of 100%, has grown by more than 60% from RM 37 million in 2010 to RM 57 million in 2013.

Source: 7-Eleven Malaysia’s IPO Prospectus

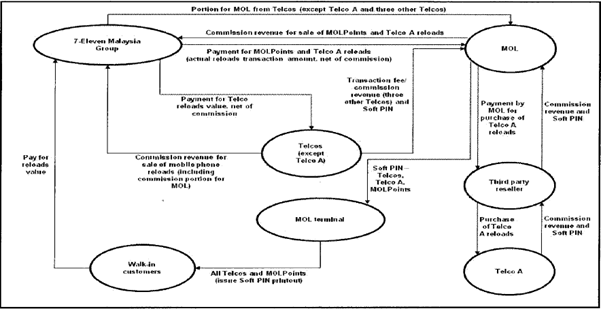

MOL Global, an e-payment platform for gaming, plays an important role in the generation of commission income for 7-Eleven. MOL Global’s largest shareholder is Vincent Tan and went through an IPO just a few months back at Nasdaq. Commission income is generated from mobile phone reload services and gaming reload done through 7-Eleven outlets. All mobile phone reload will be done through MOLReloads terminal at 7-Eleven.

Source: 7-Eleven Malaysia’s IPO Prospectus

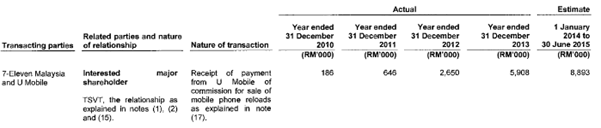

U Mobile and MOL Global accounts for 50% of the commission income earned by 7-Eleven Malaysia. U Mobile is owned by U Television which is also owned by Vincent Tan.

MOL Global – Trouble arose within months of IPO

Let’s sidetrack from the discussion of 7-Eleven and looked at MOL Global which was recently listed in October, 2014. 1 month after the IPO, MOL Global announced that the CFO has resigned and the 3rd quarter financial results will be delayed . During the IPO road show, was the management unaware of the possible delay of financial result reporting?

In December 2014, it was then disclosed that their Vietnam unit has overstated revenue and MOL Global’s net profit tumbled by 61.5% in the 3Q results. This must have been the fastest discovery of overstatement of financial statement from the day of IPO. A class action has now been filed against MOL Global for making false and misleading statements .

From the IPO price of $12.50, investor will have lost 80% in 2 months

If we traced back the history of MOL Global, it was actually listed in 2003 as MOL AccessPortal on the MESDAQ of Malaysia Stock Exchange before it was privatized in 2008. The listing price was RM 0.75 per share and the company was delisted at RM 0.62 per share . The same pattern of listing and delisting is common among Vincent Tan’s related companies. With the sharp fall in share price of MOL Global, do not be surprised if it got privatized again.

The author Shan Rui started his investment journey in September 2011 and has been a steadfast believer of the philosophy of value investing. Over the past 3 years, he has witnessed and experienced the danger of investing in Asia’s capital market. As a passionate investor, he hopes to improve the awareness and understanding of the public, so that they can better navigate through the smoke and mirrors.