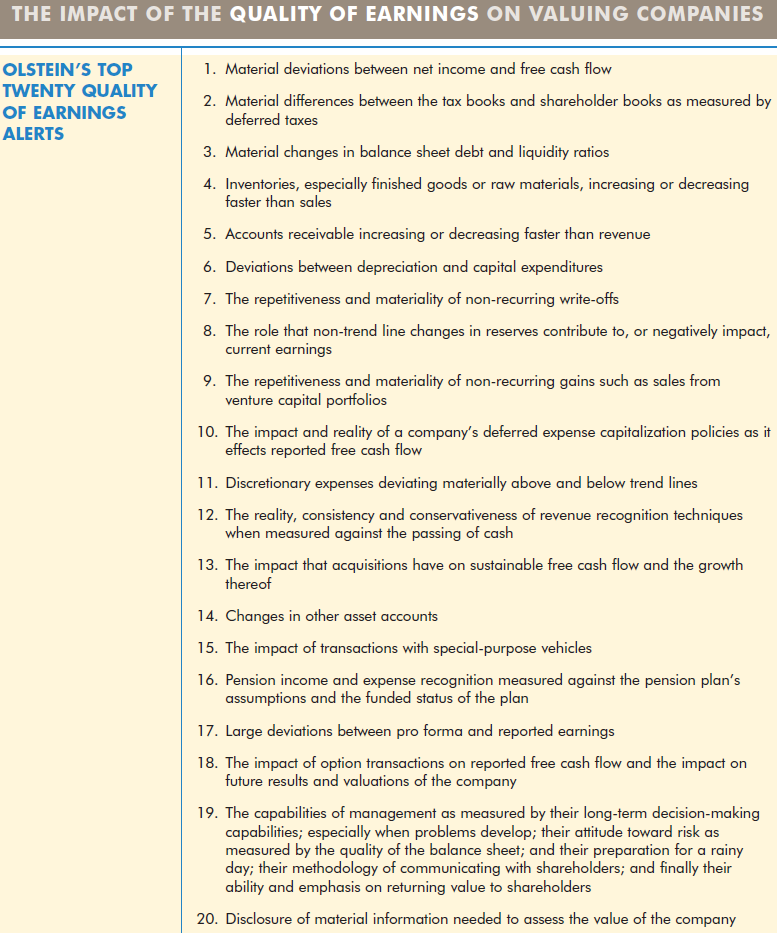

Olstein’s Top 20 Quality of Earnings Alerts

Olstein Funds: Accounting Alerts Help Avert Trouble

An astute investor should be aware of the types of accounting smokescreens that companies use to disguise problems and to misrepresent the company’s economic reality. The following alerts are sometimes clear indicators of future earnings surprises and have proved valuable to investors:

Journal of Corporate Finance Volume 31, April 2015, Pages 220–245

Family control and corporate cash holdings: Evidence from China

Qigui Liu , Tianpei Luo , Gary Gang Tian,

Highlights

Abstract

This study examines the effect of family control on the cash holding policy in China. We find that family firms with excess control rights tend to have high cash holdings that are tunneled rather than being invested or paid to shareholders. We further show that the incentive for controlling families to hold cash and for tunneling is exacerbated by the agency conflict between controlling and minority shareholders, i.e., it is weakened after the Chinese Non-tradable share (NTS) reform and strengthened by the presence of multiple large shareholders who probably play no monitoring role in Chinese family firms. Furthermore, family firms’ incentive to hold cash for tunneling is influenced by the unique characteristics of Chinese firms in the following ways: the incentive is stronger when the family founder has one child and face family succession problem, and when the founder has political connections and directly involves in firm’s management; while it is weakened by family founder’s social interpersonal trust with other entrepreneurs through their membership of Chambers of Commerce. Overall, we argue that family firms in China tend to hold high levels of cash for tunneling, which harms firm value, while the severe controlling-minority shareholder agency conflicts and unique Chinese family characteristics only make this situation worse.

http://www.valuewalk.com/2015/04/james-montier-who-is-cooking-the-books-the-c-score

James Montier: Who Is Cooking The Books – The C-Score

Posted By: Guest PostPosted date: April 16, 2015 02:09:30 PMIn: Value InvestingNo Comments

James Montier: Who Is Cooking The Books – The C-Score via Value Investing Insight

In good times, few focus on such ‘mundane’ issues as earnings quality and footnotes. However, this lack of attention to ‘detail’ tends to come back and bite investors in the arse during bad times. There are notable exceptions to this generalization. The short sellers tend to be amongst the most fundamentally driven investors. Indeed, far from being rumor mongers, most short sellers are closer to being the accounting police. To aid investors in assessing the likelihood of accounting shenanigans, I have designed the C-score. When combined with measures of overvaluation, this score is particularly useful at identifying short candidates. Continue reading

Review of Quantitative Finance and Accounting

May 2015, Volume 44, Issue 4, pp 791-815

Stock manipulation and its effects: pump and dump versus stabilization

Abstract

This study examines the manipulation of stock prices in Taiwan stock markets. Using a new set of hand-collected data, we examine the characteristics and patterns of manipulated stocks and their effects on the market. Our results show that manipulated firms tend to be small and to have poor corporate governance. Most manipulation cases involve a “pump-and-dump” trading strategy and stabilization operations. Pump-and-dump manipulations lead to high temporary price impacts, increased volatility, large trading volumes, short-term price continuation, and long-term price reversals during the manipulation period. They therefore have an important impact on market efficiency. In stabilization cases, the manipulation has no impact on market performance, except that the price drop and abnormal returns of the post-manipulation period are significantly lower than during the pre-manipulation period. Firm fundamentals are important in deciding the price impacts of stock manipulation. Compared with manipulated firms with positive fundamentals, the manipulation of firms with negative fundamentals has a more detrimental effect on market efficiency.

Earnings Management and the Long-Run Underperformance of Firms Following Convertible Bond Offers.

Chou, De-Wai1 Wang, C. Edward1 Chen, Sheng-Syan1 Tsai, Sandra1

Journal of Business Finance & Accounting. Jan/Feb2009, Vol. 36 Issue 1/2, p73-98. 26p. 9 Charts.

Abstract:

This paper examines whether the long-run underperformance of convertible bond issuers can be explained by earnings management, as reflected in discretionary current accruals around the time of the offer. Consistent with the earnings management hypothesis, we find that convertible issuers who adjust their discretionary current accruals to report higher net income in the issue year will generally experience inferior operating and stock return performance over the five-year post-issue period. Our findings indicate that there is some temporary overvaluation of convertible issuers by the stock market, but that the resultant disappointed investors will subsequently correct their valuation errors. The similarity of our results to those reported within the prior literature on initial public offers (IPOs) and seasoned equity offers (SEOs) suggests that the earnings management hypothesis is not unique to stock offers, but that it actually extends to convertible bond offers.

Journal of Banking & Finance Volume 55, June 2015, Pages 92–106

Protection or expropriation: Politically connected independent directors in China

Abstract

This paper empirically investigates politically connected independent directors among Chinese listed firms using 7487 firm-year observations from the Shanghai stock exchange during the period of 2003–2012. We distinguish between privately controlled firms and state-controlled firms. We find that the value effect and incentives of appointing independent directors with political ties are shaped by a firm’s ownership structure. More exactly, Chinese listed privately controlled firms with a large fraction of politically connected independent directors tend to outperform their non-connected counterparts, due to the ease of access to external debt financing and more subsidies from the government. However, the appointment of politically connected independent directors also enlarges the magnitude of related-party transactions with the controlling party in listed privately controlled firms. In contrast, having politicians as independent directors does not help to add value to listed state-controlled firms, especially firms controlled by the local government, due to the expropriation of minority investors via more related-party transactions and more severe over-investment problems.

Journal of Accounting and Economics Volume 60, Issue 1, August 2015, Pages 36–55

Market (in)attention and the strategic scheduling and timing of earnings announcements

Ed deHaana, , Terry Shevlinb, , , Jacob Thornockc,

Abstract

We investigate whether managers “hide” bad news by announcing earnings during periods of low attention, or by providing less forewarning of an upcoming earnings announcement. Our findings are consistent with managers reporting bad news after market hours, on busy days, and with less advance notice, and with earnings receiving less attention in these settings. Paradoxically, our findings indicate that managers also report bad news on Fridays, but we do not find lower attention on Fridays. Further, we find negative returns when the market is notified of an upcoming Friday earnings announcement, which is consistent with investors inferring forthcoming bad news.

Does Internal Audit Function Quality Deter Management Misconduct?

Ege, Matthew S.1

Accounting Review. Mar2015, Vol. 90 Issue 2, p495-527. 33p. 7 Charts.

Abstract:

Standard-setters believe high-quality internal audit functions (IAFs) serve as a key resource to audit committees for monitoring senior management. However, regulators do not enforce IAF quality or require disclosures relating to IAF quality, which is in stark contrast to regulatory requirements placed on boards, audit committees, and external auditors. Using proprietary data, I find that a composite measure of IAF quality is negatively associated with the likelihood of management misconduct even after controlling for board, audit committee, and external auditor quality. This result is robust to a variety of other specifications, including controlling for internal control quality and separate estimation during the pre- and post-SOX time periods. A difference-indifferences analysis indicates that misconduct firms have low IAF quality and competence during misconduct years and improve IAF quality and competence in the post-misconduct years. These findings suggest that regulators, audit committees, and other stakeholders should consider ways to improve IAF quality