http://www.wsj.com/articles/hanergy-is-still-a-head-scratcherheard-on-the-street-1427785577

Hanergy Is Still a Head Scratcher

ABHEEK BHATTACHARYA

Updated March 31, 2015 4:44 a.m. ET

For anybody who expected big numbers out of the world’s most valuable clean energy company, Hanergy Thin Film Power didn’t disappoint. The Chinese solar company whose shares have vaulted 450% in the past year reported late Monday that its 2014 revenue nearly tripled, and net profit rose 64%. As common as these numbers might start to look, though, they are still strange. Hanergy makes equipment to build niche kinds of solar panels that are either so inefficient that they have been abandoned by peers, or so new that the economics are untested. How this business commands a $36 billion market value, more than Tesla’s, raises doubts.

A closer look at Hanergy’s 2014 results keeps raising doubts, too. Out of $1.2 billion of revenue in 2014, 62% comes from selling equipment to its closely held parent, Hanergy Holding Group, who then builds solar panels. But much of what goes to the parent seems to come back, since between 2015 and 2017, the parent plans to sell panels back to listed Hanergy worth as much as $6.1 billion, according to separate filings in February.Most of the remaining revenue last year came from selling solar power-station assets to an investment fund called Beijing Hongsheng Photovoltaic Industry. Yet there are some doubts about Beijing Hongsheng’s status. The legal representative of the ultimate shareholder of Hongsheng appears to be the wife of a former independent Hanergy director, according to documents reviewed by The Wall Street Journal. Hanergy has denied that the asset disposals were connected-party transactions.

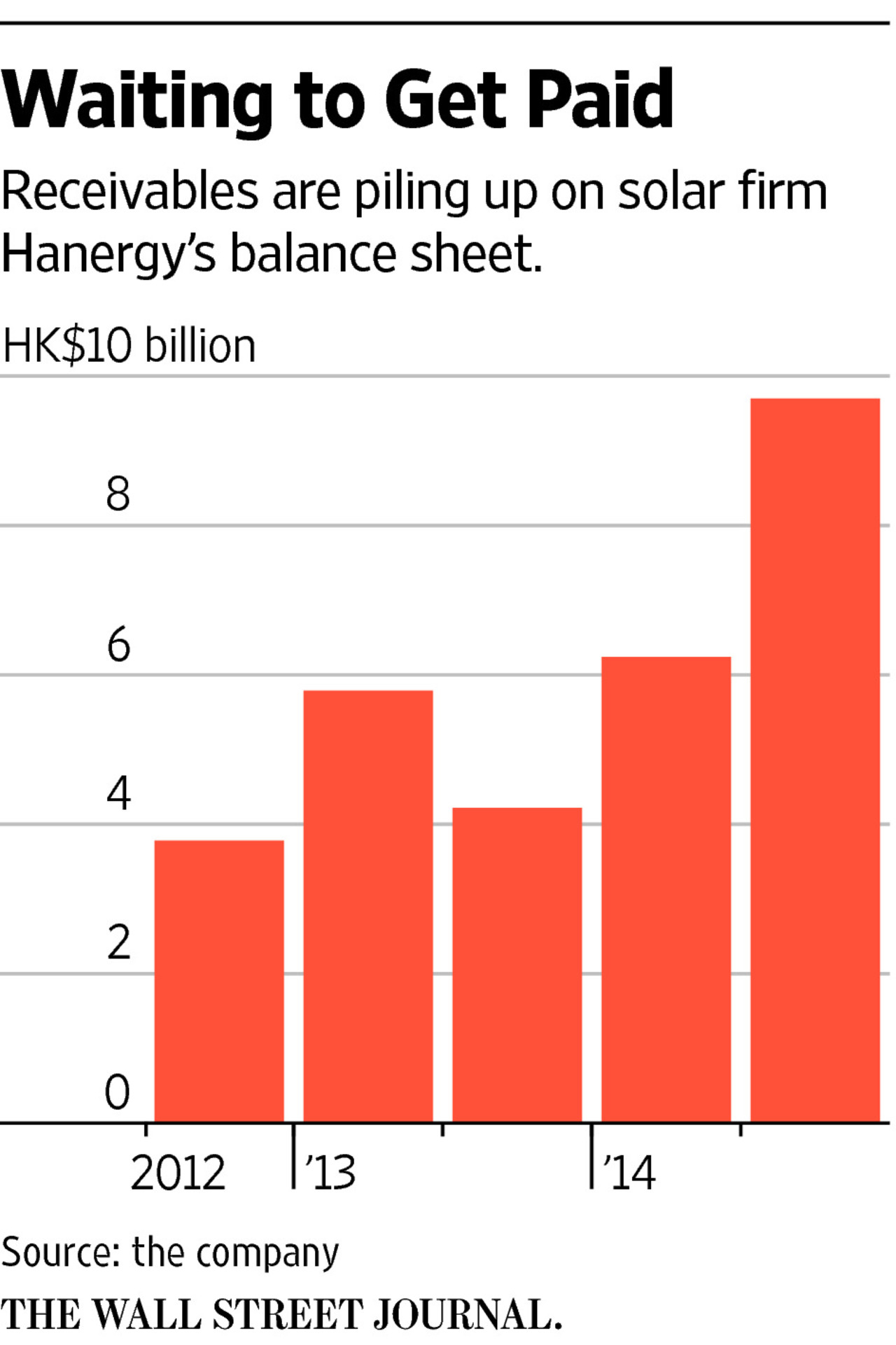

And these parties aren’t always paying Hanergy in cash on time. Receivables on the balance sheet at the end of 2014 more than doubled from a year before, most of them related to its parent. These were equivalent to 101% of revenue in 2014. The company didn’t publish a cash-flow statement.

One change from previous reports: Profitability is slipping. The net profit margin in the second half of 2014 clocked 24.6%, down from 54% in the first half and 69% in 2013. Perhaps the margins are naturally declining as costs rise in a growing business, but they remain higher than at peers. New York-listed First Solar managed 15% between July and December, and Hong Kong-listed GCL-Poly Energy 5.3%.

Hanergy shares ended Tuesday nearly 4% higher. One could that say the stock’s performance just reflects these results. Or, that both the shares and the underlying financials leave investors scratching their heads.