http://www.wsj.com/articles/nobles-spat-with-iceberg-highlights-barriers-to-disclosure-1425932989

Posted by John SOH Yong Ye, Year 4 undergrad at the School of Economics, Singapore Management University

Noble’s Spat With Iceberg Highlights Barriers to Disclosure

Commodity traders become more open, but there are limits

Noble Group is a middleman in commodities markets. PHOTO: REUTERS

ANDREW PEAPLE

March 9, 2015 4:29 p.m. ET

HONG KONG—Once renowned for their secretive nature, companies that make billions of dollars shifting commodities around the world have been slowly emerging into the limelight in recent years. But a high-profile scrap between Hong Kong-based Noble Group Ltd. and Iceberg Research, a little-known research firm, has pointed up a persistent problem: It can be hard to tell how trading companies make their money.While Iceberg hasn’t accused Noble of fraud, it argues the trader “stretches accounting rules to the maximum,” and has queried the way Noble accounts for its ongoing contracts and its holdings in other companies.

Noble has consistently rejected Iceberg’s claims. After it issued a rebuttal late Thursday its shares rose 6% in Singapore on Friday, though they slipped back 4.4% on Monday. But the trader has admitted it needs to do more to communicate how well it is performing.

The issue for Noble, and other listed trading companies such as Glencore PLC or BungeLtd. , is how much they can realistically disclose to back up their published financial statements.

As Noble noted in its rebuttal to Iceberg, the company has around 12,000 contracts with commodity producers and customers. Noble also has a substantial number of long or short positions in derivatives, bets that would benefit it if prices rose, or fell, used to hedge its commodity holdings.

Trading companies could be put at a competitive disadvantage if they disclose too much, as rivals seek to emulate or better the deals they have done.

ENLARGE

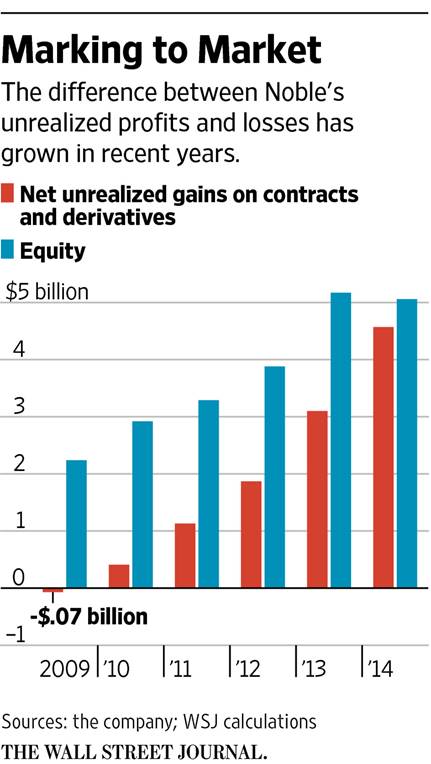

Iceberg argues that the scale of unrealized profits recorded by Noble on its derivatives contracts—the overall net gain at the end of last year was $4.6 billion, equivalent to 90% of its equity—is evidence that the valuations the trading firm is using have reached “incredible” levels.

Noble says much of the unrealized gains resulted from a big swing in the value of oil futures it uses to hedge its stocks of crude: As oil prices fell, its short futures position jumped in value. But it won’t say exactly how much of a profit it earned as a result.

Trading firms’ hesitancy to disclose much about their wins and losses in the market mean it can be much harder for an outsider to understand a set of accounts for a company like Noble than, say, for straightforward mining companies like Rio Tinto PLC or BHP Billiton PLC.

“You can model a mining company to a high degree of accuracy,” says Paul Gait, mining analyst at Sanford C. Bernstein in London. “But for traders, going into the detail of the business requires a level of disclosure they don’t give you, and which practically they can’t.”

“There is an element of trading companies having to say ‘trust me’,” Mr. Gait said.

Compared with global banks, which have a number of regulators breathing down their necks, trading companies remain relatively unregulated. In Noble’s case, its accounts and the procedures used to produce them are checked by Ernst & Young.

“You just have to trust the auditors,” says Mr. Gait. Ernst & Young has declined to comment on the debate regarding Noble.

Another difficulty for investors is that the trading firms themselves have become quite varied. Iceberg, for example, has pointed to differences in Noble’s financial position to that of rival Glencore as further evidence of problems.

But following its merger with mining company Xstrata PLC in 2013, Glencore is a rather different beast from Noble. Whereas Noble operates an “asset-light’”operation, owning few properties but mainly acting as a middleman in commodities trading, Glencore owns plenty of mines, oil rigs and storage facilities. About 60% of its operating profit comes from these production-related assets, making Glencore ever more similar to a pure resource company like BHP or Rio.

In turn, some say, that makes Glencore—a former partnership that listed in 2011—more suitable for the public markets. With a listing, long-term assets such as mines and other infrastructure can be backed by longer-term equity funding.

“When you move to more a mining model, it pushes you to a public ownership model,” says Craig Pirrong, professor of finance at the Bauer College of Business, University of Houston.

But, says Mr. Pirrong, companies like Noble that are more like pure traders, and which manage their risk through buying and selling derivatives, could be better off remaining as partnerships. “The companies that have had issues are all asset-light trading firms that are publicly owned,” he says.